3 mobile tactics digital banks use to win

TL;DR

- Digital banks grow 50% annually while traditional banks struggle with mobile engagement despite superior customer relationships and trust

- Behavioral segmentation recovers 15-25% of abandoned onboarding and increases conversion 30-40% by triggering marketing at moments of intent

- Deep linking achieves 3-5X conversion lifts by eliminating friction between campaigns and app destinations

- Measurement infrastructure proves ROI and enables budget reallocation based on evidence rather than guesswork

- Most banks see positive ROI within 30-60 days when implementing these three tactics together

The mobile engagement gap in banking

Your bank texts you: “$127.50 debited from your account.” You don’t recognize the amount. You tap the link to see what it was. The app opens to your home screen. Now you’re scrolling through transactions trying to find that specific charge. Was it groceries? That subscription you forgot about? Digital banks send the same text, but tapping opens directly to that exact transaction. Instant clarity.

This friction point illustrates a larger problem. Digital banks have increased mobile engagement rates by nearly 50% by mastering what traditional banks struggle with: converting app downloads into active, engaged users. The gap doesn’t stem from marketing budgets. It comes from three interconnected capabilities that turn mobile channels into measurable growth engines.

In this article, we’ll reveal those three strategies and why traditional banks’ greatest assets (established customer bases, decades-proven trust, and regulatory mastery) sit underutilized without them.

Here’s how traditional banks can close the gap with three proven tactics:

1. Build behavioral segments that trigger at the right moment

Traditional banks organize marketing around demographics: age, income, account type. These describe identity but reveal nothing about immediate needs or optimal timing.

Digital banks segment around behavior and intent, dramatically improving conversion because messaging reaches customers actively considering the next step.

Starling Bank’s growth to 4.6 million accounts demonstrates this approach. When a customer purchases coffee, the transaction generates confirmation. Many tap to review, creating a moment of financial awareness. Starling presents an option to automatically save the round-up, which requires enabling with one tap. The purchase creates the marketing moment, the app open becomes the conversion, and feature activation establishes ongoing usage.

When customers already have finances front-of-mind, relevant suggestions convert at dramatically higher rates. For marketing teams, this increases feature adoption without increasing budget because timing does the heavy lifting.

Three high-value segments deliver immediate impact:

- Customers who started onboarding without completion typically see 15-25% recovery with targeted messaging addressing barriers. One bank achieved 23% recovery within two months, reducing wasted marketing spend by converting prospects who already expressed interest.

- Customers who activated accounts but executed zero transactions within the first week show 30-40% conversion increases when teams highlight features or offer modest incentives. Early activation drives long-term retention.

- Customers exploring product features without completing activation see 3-5X improvement in completion with simplified workflows, revealing where friction exists and justifying investment in streamlined experiences.

Implementation starts with existing data so you’ll need to:

- Refine targeting based on what converts

- Map your customer journey for one product – personal loans, savings accounts, or credit cards.

- Identify drop-off points using current analytics.

- Create three behavioral segments based on these friction points: abandoned applications, activated but dormant accounts, and feature browsers.

- Use your marketing automation platform to trigger relevant messages when customers exhibit these behaviors.

- Test messaging that addresses specific barriers (“Need help completing your application?”) against generic reminders.

- Measure recovery rates, activation rates, and feature adoption for each segment.

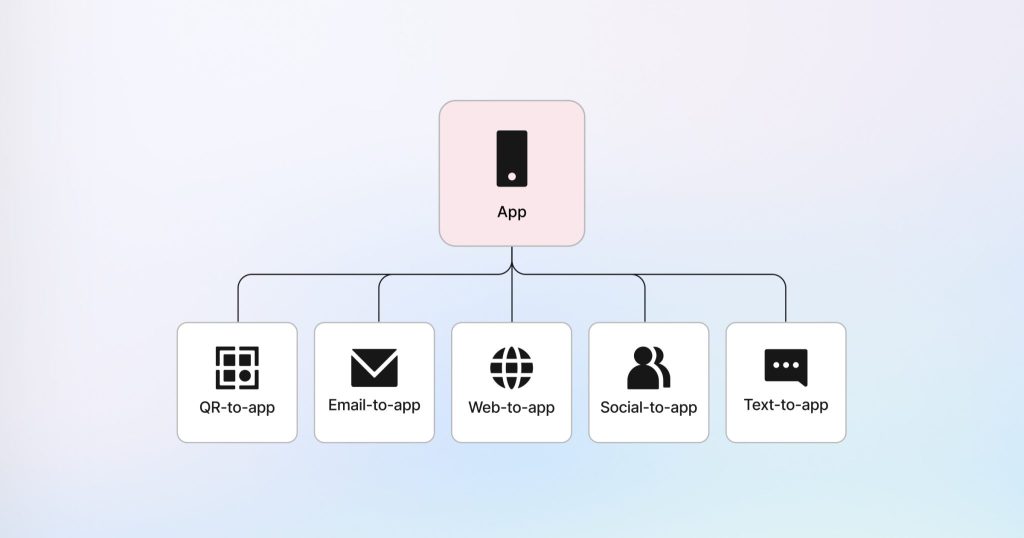

2. Connect every campaign directly to the intended destination

A customer receives an email promoting a savings account. There’s clear value and a compelling call-to-action. Interested, the customer taps but the app launches on the generic homescreen showing balances and menus instead of on the page reflecting content related to a savings account.

As a result, the customer must remember why they opened the app and navigate without guidance. A sub-par user experience often leads to closing the app, while marketing teams see impressive click-through rates but poor conversion. Monzo systematically eliminates this experience through deep linking. For example, when a Monzo customer taps from email highlighting budgeting, the app launches directly at the budget interface. The screen displays exactly what the email described. Setup requires only two taps.

Deep linking delivers three compounding advantages.

- Conversion rates improve dramatically – data across banking implementations shows typical lifts of 3-5X for feature adoption and 2-3X for account funding.

- Customer experience improves uniformly across channels, building trust and reducing abandonment.

- Granular performance measurement provides visibility generic analytics cannot deliver. When teams see email campaigns converting at 8% while SMS converts at 3%, budget reallocation becomes obvious.

Axis Bank also achieved 25% month-over-month lift in downloads after implementing deep linking alongside measurement infrastructure by fixing specific friction points.

Text-to-app delivers similar impact for time-sensitive communications. SMS achieves 98% read rates. When customers receive fraud alerts or payment reminders, deep links route them directly to the relevant screen: the exact transaction for review, the payment screen ready to submit, or the declined card with instant resolution options. This turns urgent moments into completed actions instead of support calls, reducing operational costs while improving customer experience.

We recommended prioritizing highest-volume campaign types such as feature adoption emails, account funding reminders, and card activations to make the most of deep linking. These campaigns already have volume, making user experience improvements visible much faster. The bottom line is that modern deep linking accommodates compliance requirements while maintaining audit trails, with most banks seeing positive ROI within 30-60 days.

3. Implement measurement infrastructure connecting spend to outcomes

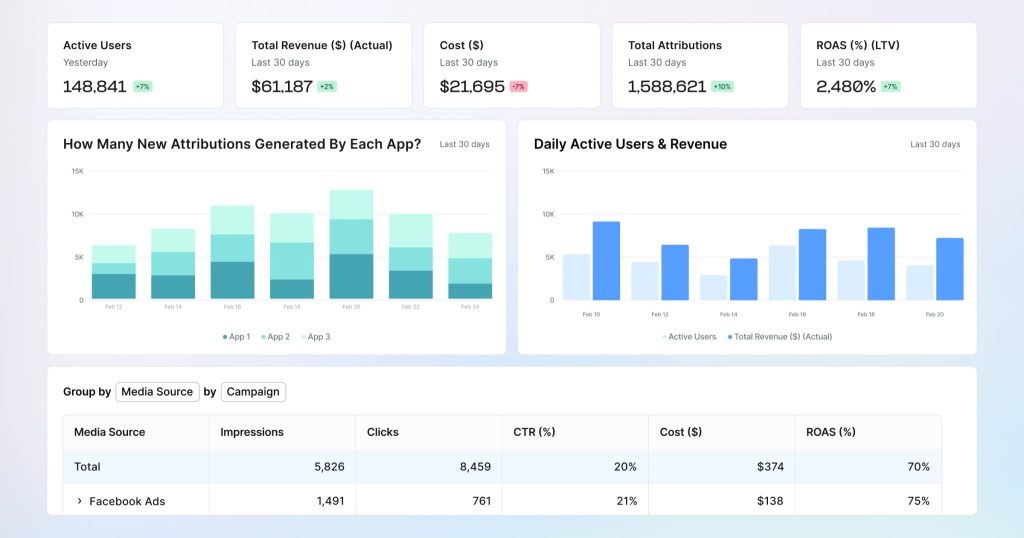

Traditional bank marketing teams face a familiar scenario. Campaigns run, generating install volumes. Leadership asks: “Which channels bring customers who fund accounts?” The answer requires exporting data from three systems, manually aligning identifiers, guessing at attribution. By the time analysis completes, budgets have been reallocated.

The issue isn’t insufficient data. Banks drown in it. The challenge is infrastructure that transforms fragmented metrics into actionable intelligence.

Digital banks built measurement as foundational infrastructure, unifying every customer interaction in accessible dashboards. Marketing identifies which campaigns convert prospects into customers; product teams pinpoint features that drive retention; finance calculates channel-level profitability. And on top of it there’s one dataset that powers every decision.

Consider the quarterly review scenario. A social media campaign delivered 10,000 app installs at an attractive cost per install (CPI). Marketing celebrates efficiency. Leadership probes deeper: How many customers completed account setup? What percentage made their first deposit? How does 90-day retention compare across acquisition sources? Without connected infrastructure, teams optimize surface metrics while missing what actually drives value.

Digital banks approach measurement through a revenue lens. They prioritize events with direct business impact: first-week account funding, 30-day card activation, and initial transaction completion. These signals reveal which marketing efforts generate valuable customer behaviors, enabling confident budget shifts toward proven performers.

Building effective measurement requires three foundational capabilities.

1) Unified attribution systems connect campaign origins to in-app behavior and business outcomes. This captures end-to-end customer journeys including web-to-app transitions and QR code interactions, eliminating visibility gaps between marketing investment and revenue generation.

Traditional banks often rely on platform-reported last-touch attribution. One institution discovered three separate channels claiming credit for identical conversions, driving budget allocation based on inflated performance rather than true contribution.

2) Event-level data exports that integrate with existing business intelligence infrastructure form the second requirement. When measurement platforms deliver raw data feeds, analytics teams merge mobile performance with customer lifetime value models and profitability calculations already powering bank operations. This transforms measurement from isolated marketing reporting into enterprise-wide strategic insight.

3) Standardized event definitions measured consistently across iOS, Android, and web. This unified data foundation means marketing growth metrics align with product engagement reports and finance performance tracking. When one European bank implemented this consistency, analysis revealed 30% of digitally-attributed new accounts were existing customers opening additional products. Refined targeting based on this insight recovered 15% of acquisition spending.

The required infrastructure already exists. ISO-certified, GDPR-compliant, SOC 2 Type II platforms built specifically for financial services deliver sophisticated measurement within regulatory boundaries. Built-in fraud detection filters invalid installations and click manipulation, protecting budgets from wasted spending.

Practical implementation begins with partner selection:

- Choose a mobile measurement platform meeting banking security standards.

- Follow a systematic integration approach. Install their SDK in your mobile banking application to capture core events: installation, registration completion, first transaction.

- Integrate with major advertising platforms enabling Facebook and Google to optimize toward quality outcomes rather than raw installation volume.

- Establish three to five key performance indicators leadership actually monitors: cost per funded account, 90-day customer retention, digital product adoption percentage.

- Create a unified performance dashboard combining measurement platform data with internal customer information. Marketing, product, and finance teams reference identical metrics.

- Launch one pilot campaign leveraging this infrastructure: perhaps a credit card offer where you measure not just applications but approval rates and first purchase behavior.

- Demonstrable results justify broader rollout.

The measurement infrastructure advantage

Success in mobile banking doesn’t separate on talent or technology availability. It hinges on treating measurement as essential infrastructure rather than periodic reporting exercise.

These three capabilities create compounding value. Measurement infrastructure proves which channels drive valuable customers. Behavioral segmentation ensures relevant messages reach receptive customers at optimal moments. Deep linking preserves momentum by eliminating friction.

When combined, a 20% lift in targeting, 3X improvement from friction elimination, and efficient budget allocation compound substantially. Digital banks embedded this infrastructure from founding but operate from weakness: zero customers and minimal trust, spending billions to acquire what established banks already possess.

Traditional banks possess millions of relationships, brand recognition, and regulatory credibility. The question isn’t whether to adopt these tactics. It’s whether institutions will invest in the infrastructure to leverage existing advantages before the window closes.

Implementation approach

Month one: Map customer journeys for priority products. Assess measurement capabilities.

Month two: Deploy measurement infrastructure. Build one behavioral segment with attribution. Implement deep linking for highest-volume campaigns.

Month three: Analyze systematically. Expand measurement. Add deep linking. Reallocate budget based on evidence.

The closing window

Digital banks like Starling (4.6 million accounts) and Monzo execute these three tactics daily while growing 50% annually. They built measurement infrastructure from founding, proving impact and securing continued investment.

Traditional banks have established customer relationships and proven trust, but that advantage erodes every quarter without infrastructure to leverage it. Most banks see positive ROI within 30-60 days. Banks implementing now prove mobile ROI to leadership and secure budget. Competitors who delay remain stuck defending spend with incomplete data.

The window for competitive advantage is closing. Banks moving first will demonstrate measurable outcomes while others explain why they can’t connect marketing spend to revenue.

Ready to close the mobile engagement gap? Speak to our mobile banking experts to learn how AppsFlyer’s financial services solutions can help you implement these tactics.

Key takeaways

- Behavioral segmentation targeting actions like “viewed loan calculator 3 times” outperforms demographic targeting by 3-5X

- Deep linking eliminates 50-70% of conversion loss that happens between campaign tap and app destination

- Measure business outcomes your CFO cares about; account funding, card activation, transaction completion, rather than vanity metrics

- The three tactics compound: a 20% targeting lift combined with 3X friction reduction plus efficient budget allocation creates substantially larger impact

- Prioritize highest-volume campaigns like feature adoption emails and card activation for fastest ROI

- ISO-certified, GDPR-compliant platforms designed for banking remove regulatory concerns as implementation blockers

Frequently asked questions

The three tactics are behavioral segmentation (targeting customers based on actions rather than demographics), deep linking (connecting campaigns directly to specific app destinations), and measurement infrastructure (proving which efforts drive business outcomes like account funding). They work together to improve conversion while proving ROI.

Traditional banks target by age and income. Behavioral segmentation targets by actions like “viewed investment features three times” or “completed first purchase today.” This reaches customers when they’re actively considering next steps, which is why it increases feature adoption without increasing budget.

Banks typically see 3-5X conversion lifts for feature adoption and 2-3X for account funding. The improvement comes from eliminating friction between what the campaign promised and where customers land in the app.

Three components: unified systems that link campaigns to business results across web and app, raw data that integrates with your existing BI tools, and consistent event definitions across iOS and Android. This gives leadership a single source of truth when evaluating mobile ROI.

Traditional banks already have millions of customer relationships and decades of brand trust. Digital banks start with zero customers and spend billions acquiring what you already possess. The question is whether you’ll invest in infrastructure to leverage your existing advantages.