Las 5 tendencias de datos que marcaron el marketing de aplicaciones móviles en 2021 y qué significan para 2022

El 26 de abril de 2021 pasará a ser una de las fechas más importantes de la historia del marketing digital.

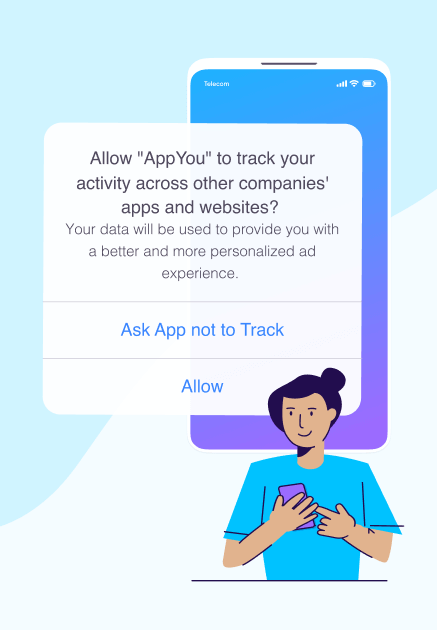

Ese día, Apple comenzó a aplicar su marco de App Tracking Transparency (ATT) en iOS 14.5, requiriendo que las aplicaciones obtengan activamente el consentimiento del usuario para el seguimiento a través de un mecanismo de opt-in, marcando el comienzo de una nueva era de privacidad.

Si bien es cierto que fue una medida bien recibida en lo que respecta a la privacidad de los consumidores, la ATT creó un enorme desafío para los mobile marketers. De repente, los datos eran en su mayoría limitados y agregados, lo que ponía patas arriba la medición y la optimización basadas en el nivel del usuario.

Los temblores se hicieron sentir en todo el ecosistema: desde los marketers de aplicaciones, pasando por las fuentes de medios y las redes publicitarias, hasta los proveedores de atribución y medición móvil.

¿Cómo influyó la ATT en el número de descargas impulsadas por el marketing? ¿Sigue siendo el remarketing una actividad de marketing viable? ¿Cómo ha cambiado la asignación de presupuestos y cuál ha sido el efecto en el gasto de los consumidores en aplicaciones?

Para abordar estas cuestiones, nuestro reporte anual sobre las 5 principales tendencias de datos analizó más de 60.000 millones de instalaciones de apps en 2021, lo que nos permite predecir lo que nos deparará 2022 a medida que el sector siga adaptándose al nuevo paradigma de la privacidad.

Haz clic en los siguientes enlaces para navegar:

Todos los datos utilizados en el reporte son medidos por AppsFlyer, la plataforma de medición y experiencia de marketing. Esto se hace a través de las integraciones con los principales socios de medios, así como su SDK propietario implementado en las aplicaciones de sus clientes. Todos los datos son anónimos y agregados.

1) Instalaciones: Las capacidades de medición de marketing se conservan en gran medida tras el descenso inicial posterior a iOS 14.5

Se ha hablado mucho de cómo la COVID-19 aceleró significativamente la transformación digital en 2020.

Sumándose a la tendencia de digitalización, nuestros datos muestran que también se ha creado una nueva normalidad en el mundo de las aplicaciones móviles, con toda la línea de base de instalación y uso elevada en 2021, como podemos ver en el siguiente gráfico.

Una comparación interanual hace que las instalaciones de 2021 superen a las de 2020 en un 19%. Esto es toda una hazaña teniendo en cuenta que 2020, con sus políticas de bloqueo y distanciamiento social, generó un salto del 33% en comparación con 2019.

El aumento del consumo digital de los dispositivos móviles en 2021 fue un gran punto de partida para el espacio de las aplicaciones móviles.

Pero el 26 de abril, iOS 14.5 de Apple cambió la forma de jugar.

Como se ha visto anteriormente, las instalaciones generales de aplicaciones aumentaron, lo que puede medirse fácilmente. El problema de magnitud fue, inicialmente, la dificultad para medir las instalaciones no orgánicas (NOI) y deducir los datos de múltiples fuentes:

- SKAdNetwork (SKAN): Atribución realizada en el propio dispositivo por el mecanismo de atribución centrado en la privacidad de Apple.

Y la atribución tradicional realizada para:

- Usuarios con consentimiento de la ATT: Atribución basada en la coincidencia de ID. Vale la pena mencionar que, aunque los índices de consentimiento fueron más altos de lo previsto, la mayoría de los usuarios no pudieron ser atribuidos con la coincidencia de ID, ya que requiere un doble consentimiento (más adelante hablaremos de ello).

- Usuarios sin consentimiento: Atribución basada en los modelos agregados de AppsFlyer – Marco de Privacidad Avanzada Agregada para los medios de pago o modelos probabilísticos para los medios propios.

- Usuarios de versiones anteriores: Aquellos que aún no han actualizado a iOS 14.5+.

Para la deduplicación, utilizamos el valor más alto de NOI por fuente de medios y campaña en cada semana medida, lo que explica que la cifra global sea inferior a la suma de los datos tradicionales y de SKAdNetwork.

Al principio, la atribución tradicional se vio afectada, con una caída del 25% hasta el 21 de junio y un 5% más hasta mediados de septiembre. En cuanto a SKAN, las cosas tampoco parecían ir mejor al principio, con una adopción e implementación lentas entre los anunciantes y las empresas de medios.

Aunque el tráfico de SKAN empezó a subir en julio, la atribución tradicional siguió siendo baja. Sin embargo, con el paso del tiempo, la innovación empezó a funcionar a medida que invertíamos importantes recursos en mediciones alternativas y respetuosas con la privacidad.

Está claro que ganar crédito para los NOIs este año ha sido difícil para los marketers de iOS, con una caída general del 5% (mientras que los NOIs de Android aumentaron un 15%).

Pero:

En los últimos dos meses, la atribución tradicional se aceleró, aumentando un 17%. Con la adopción continuada de SKAN, las capacidades de medición se han mantenido en gran medida con el número de NOIs atribuidos acercándose a los niveles anteriores a iOS 14.5.

Los juegos adoptan SKAN pero reciben un golpe por su dependencia del marketing

Podemos ver que las aplicaciones de juegos, conocidas por su agilidad y conocimiento de los datos, han adoptado SKAN mucho más rápido que las aplicaciones que no son de juego, con un 67% de NOIs frente a un mero 30%.

Pero una visión general muestra que las limitaciones de datos y los cambios de medición han afectado a las aplicaciones de juegos. Basándonos en el análisis de más de 100.000 millones de instalaciones desde enero de 2020, podemos ver una caída del 6% interanual en las instalaciones de aplicaciones de juegos en 2021, mientras que las aplicaciones que no son de juegos experimentaron un aumento del 25%.

Debido a la enorme competencia a la que se enfrentan los juegos y al hecho de que la marca desempeña un papel mucho menor en esta vertical, los juegos dependen mucho más del marketing. De hecho, los marketers de aplicaciones de juegos suelen tratar a los usuarios no orgánicos como de mayor calidad que los orgánicos, ya que se destacan en la adquisición de usuarios que se basa en señales a nivel de usuario.

Sin embargo, la dependencia de los datos a nivel de usuario también significa que están más expuestos a los cambios en la forma de medir y optimizar los datos. Con el cambio hacia la medición agregada, las cifras globales de instalaciones en juegos han disminuido, sobre todo como resultado de un descenso en las instalaciones impulsadas por el marketing.

Lo que nos espera en 2022

A medida que el sector siga adaptándose a la nueva norma de privacidad, la capacidad de medir, atribuir y optimizar las actividades de marketing seguirá mejorando en iOS (y en Android cuando Google introduzca sus propias medidas de privacidad).

Las mejoras serán impulsadas por modelos mejores y más sofisticados, un mayor uso de los análisis predictivos, la experiencia adquirida en SKAN, en particular la optimización de los valores de conversión (mira más abajo para más información sobre el tema), y la innovación en todo el ecosistema.

Sólo podemos esperar que Apple añada más datos que respeten la privacidad a SKAdNetwork, especialmente los tan necesarios datos orgánicos, la información a nivel geográfica, los deep links diferidos y los datos de las campañas web-to-app y de remarketing.

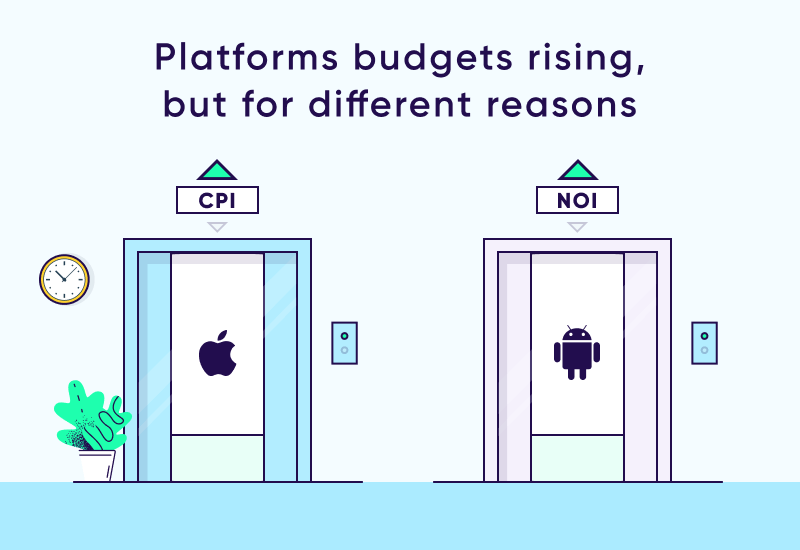

2) Presupuestos: Las apps gastarán entre 78.000 y 83.000 millones de dólares en la adquisición de usuarios en 2021, lo que supone un aumento del 40% interanual

Los presupuestos de adquisición de usuarios en 2021 alcanzarán entre 78.000 y 83.000 millones de dólares, con un rango impulsado principalmente por las estimaciones presupuestarias en China (lee el final del artículo para obtener más información sobre nuestra metodología). La cifra representa un aumento del 40% interanual impulsado por un salto del 50% en Android y un aumento del 26% en iOS.

Aunque el gasto aumentó en ambas plataformas, el motivo del crecimiento en cada sistema operativo fue totalmente diferente.

Como se ha explicado anteriormente, iOS ha registrado menos NOIs este año (-5%). Al mismo tiempo, iOS también experimentó un aumento significativo del costo efectivo por instalación, lo que impulsó los presupuestos al alza. Los precios de los anuncios aumentaron entre un 20% y un 50% en casi todas las categorías desde la entrada en vigor de iOS 14.5.

Esto significa que los marketers pudieron adquirir y obtener crédito para muchos menos usuarios por el mismo presupuesto que han invertido en 2020, o – tuvieron que aumentar su gasto para la misma cantidad de usuarios.

¿Por qué se han encarecido tanto los medios en iOS?

Para empezar, la oferta y la demanda básicas. Los precios para una oferta mucho menor de usuarios consentidos se dispararon mientras la demanda de usuarios con granularidad de datos completa se ha disparado por razones obvias.

Pero parece que la principal causa de este salto en el costo ha sido la ineficacia de los grandes medios en un momento de transición para dirigirse a las personas adecuadas y estimar el impacto correcto.

Es más difícil hacer pequeños segmentos de usuarios de alto valor, por lo que los marketers tienen que utilizar una orientación más amplia, lo que también hace que sea menos relevante.

Además, las redes aún no pueden optimizar hacia las señales in-app, aunque esta capacidad se está desarrollando con soluciones como GBRAID de Google y AEM de Facebook; hasta que no lo hagan, sus capacidades de orientación y optimización se ven afectadas negativamente.

Paralelamente, la demanda de Android con toda su granularidad de datos se disparó, con un aumento de los ingresos por ventas de más del 40% anual, especialmente en el sector de los juegos, donde los ingresos por ventas se dispararon un 50%, en comparación con el sector de apps que no son de juego, que se mantuvo en un impresionante 36%. Curiosamente, el CPI global de Android en el sector de los juegos descendió un 11% este año (aumentó un 23% en América del Norte, pero cayó un 24% y un 15% en el Sudeste Asiático y en Japón y Corea, respectivamente), mientras que el CPI en el sector no relacionado con los juegos aumentó casi un 20%.

Como se muestra en nuestro último Performance Index que incluye la primera clasificación de SKAN, los presupuestos no solo han cambiado a Android, sino que también se han desplazado entre las empresas de medios. TikTok Ads quedó en primer lugar en el Índice SKAN, mientras que Facebook ocupó el segundo lugar.

El gigante de las redes sociales también perdió su posición dominante en iOS entre los usuarios con consentimiento en favor de Apple Search Ads (ASA). El hecho de que ASA tenga su propia API y pueda mantener una granularidad total de los datos ha atraído más presupuestos a esta plataforma.

Lo que nos espera en 2022

Los presupuestos de adquisición de usuarios seguirán aumentando con más NOI en ambas plataformas. Sin embargo, el costo de los medios no aumentará tanto en iOS este año dadas las estimaciones de que las ineficiencias en el lado de la red se resolverán en gran medida.

Metodología del gasto total de la industria en UA

La fórmula combina tres buckets:

- Presupuestos medidos por uno de los principales socios de medición móviles (se hizo una extrapolación a nivel de la industria basada en estimaciones de terceros)

- Las instalaciones no atribuidas al mercado o impulsadas por el marketing que no fueron medidas por uno de los principales MMPs (alrededor del 10% según las estimaciones)

- El gasto en China, donde la medición es un desafío mucho mayor debido a la fragmentación del espacio de las tiendas de aplicaciones; utilizamos el total de App Annie de 96.000 millones de instalaciones en 2020, la tasa de NOI y CPI de AppsFlyer, y la estimación de eMarketer de la tasa del 27% de China en el gasto global en publicidad móvil.

3) Reengagement: La innovación del remarketing de pago impulsa el repunte de iOS, mientras que los medios propios aumentan un 45%

Después de una subida constante en los últimos años, los esfuerzos de remarketing de pago por parte de las aplicaciones móviles cayeron una vez que se lanzó iOS14.5. Era de esperar: sin IDFA, la segmentación y la personalización, que son la base del remarketing, no pueden funcionar.

De marzo a julio, el número de conversiones de remarketing cayó casi un 35%, a pesar de que la adopción de la versión 14.5 fue lenta (sólo un 27% en junio).

Pero entonces, como se ve en la tendencia NOI anterior, la innovación se puso en marcha, esta vez por parte de Google. El gigante de las búsquedas introdujo GBRAID, un identificador agregado y que respeta la privacidad, diseñado para optimizar las campañas de reengagement.

Dado que Google es el mayor actor en términos de volumen dentro del gráfico de remarketing, el hecho de que haya introducido una nueva forma de medir aumentó por sí solo el número de conversiones de remarketing en un 12% de julio a septiembre, y otro 14% en octubre, al comenzar la temporada de vacaciones (el año pasado, el remarketing en iOS aumentó casi un 10% en octubre frente a septiembre).

Al igual que en el caso de los NOI, Android aprovechó los desafíos de iOS, aumentando su número de conversiones de remarketing atribuidas durante todo el año en un total de más del 45%.

Los medios propios aumentan como alternativa

Con los desafíos del remarketing en iOS, no es de extrañar que el uso de los medios propios para volver a adquirir a los usuarios existentes a través de las notificaciones push, el correo electrónico y los mensajes in-app se haya disparado casi un 45% desde abril (en comparación con el aumento de solo un 17% en Android).

Además, los medios propios ofrecen a las aplicaciones una granularidad total de los datos dentro de un entorno de datos de first party (las medidas de privacidad tratan de evitar el paso de datos a terceros, no dentro de las propiedades de una empresa).

Cada vez son más las aplicaciones que utilizan herramientas integradas de segmentación de la audiencia y automatización del marketing para ayudar a los marketers de aplicaciones a volver a adquirir a los usuarios de forma eficiente. Esto les permite crear mensajes personalizados e incluso excluir a los usuarios que ya han respondido a una campaña para que no vean anuncios similares en otros canales propios.

Lo que nos espera en 2022

El reengagement seguirá impulsando un mayor uso, tanto en el lado de los datos de first party de los medios propios como en el frente del remarketing de pago, en el que las conversiones seguirán repuntando, ya que otras redes ya están trabajando en soluciones.

4) Ingresos: La dependencia de los juegos del marketing pone en evidencia sus desafíos de monetización en la era de la privacidad

Un análisis del gasto total de los consumidores (IAP o ingresos por compras in-app) en las aplicaciones muestra lo difícil que ha sido iOS14.5 para las aplicaciones de juegos.

Como sólo comparamos las aplicaciones que estuvieron activas durante todo el periodo medido, los ingresos en el sector de los juegos no suelen aumentar mucho, ya que muchos juegos tienen una vida útil limitada.

Sin embargo, una comparación entre plataformas hace que el IAP de los juegos se desplome un 38% entre abril y septiembre, frente a una caída menor del 13% en Android.

Como se ha comentado en la tendencia nº 1, a diferencia de las aplicaciones que no son de juego, los juegos dependen en gran medida del marketing y de su capacidad de optimización basada en señales de datos a nivel de usuario. Para la mayoría de los usuarios, la orientación y la optimización se han visto afectadas en su ausencia, lo que ha provocado una caída de los ingresos generales de los juegos procedentes del IAP.

La misma tendencia se observa en los ingresos por IAA (publicidad in-app) en el frente editorial, que es la otra cara de la moneda de la UA de apps de juegos. Entre abril y septiembre, los ingresos de iOS cayeron un 15%, mientras que los de Android se dispararon un 45% en el mismo periodo.

Se observan tendencias similares en las plataformas de las aplicaciones que no son de juego y que están impulsadas principalmente por el tráfico orgánico. Podemos ver un aumento en mayo, y luego una línea de tendencia de ingresos relativamente plana.

Con el mes de octubre marcando el inicio de la temporada de compras navideñas del cuarto trimestre, y noviembre en plena expansión con las ventas del Singles Day, el Black November y el Black Friday, podemos ver el impacto de las compras – la mayor categoría es la de apps que no son de juego – en la tendencia general.

Lo que nos espera en 2022

Las aplicaciones de juegos encontrarán la manera de ajustarse a los datos disponibles y a las metodologías de medición. Siempre han sido las que más rápido aprenden y, sin duda, son las que mejor se adaptan a la optimización basada en datos.

Esta vez, sin embargo, las cosas han sido más difíciles, ya que su dependencia de los datos a nivel de usuario, y también el hecho de que las redes en las que se basan también están en medio de su propia curva de aprendizaje.

5) iOS 14.5+ se profundiza en el tema: Tasas de opt-in de la ATT y mapeo del valor de conversión de SKAN

El aviso de la ATT ha cambiado por sí solo toda una industria y ha creado un gran dilema para las aplicaciones móviles. Dado que se trata de un mecanismo opt-in y una herramienta sencilla para obtener el consentimiento del usuario, las aplicaciones pueden optar por no mostrarlo. En tal caso, los responsables de marketing de aplicaciones se conformarían con la atribución de SKAdNetwork y el modelado probabilístico.

La principal razón por la que algunas aplicaciones decidieron no implementar la ATT es por la preocupación de que el aviso, con su lenguaje algo desagradable, pueda provocar la pérdida de clientes y la interrupción de la experiencia del usuario.

Pero la realidad es que los beneficios de mostrar el aviso superan con creces los beneficios de no mostrarlo.

Apoyando esta afirmación, podemos ver que seis meses después del lanzamiento de iOS14.5, casi el 65% de las aplicaciones implementaron la ATT y esperamos que este número aumente al 70%-75% el próximo año.

¿Por qué la mayoría de las aplicaciones muestran el aviso?

Pues bien, en los últimos meses hemos visto que las tasas de opt-in de la ATT alcanzan el 46%. Esto significa que en casi 1 de cada 2 casos en los que un usuario ve una solicitud, se pulsa el botón “Permitir”.

Desde el punto de vista de la experiencia del usuario, esta cifra es bastante prometedora y muestra que muchos usuarios están dispuestos a aceptar el seguimiento a cambio de una experiencia más personalizada.

Aunque ciertamente hay muchas cosas que se pueden hacer para aumentar las tasas de opt-in, cuando incluimos a los usuarios restringidos y a los usuarios que activaron la opción de limitar el seguimiento de anuncios (LAT), la tasa global se reduce, ya que Apple no permite que se muestre el aviso a estos segmentos.

Y lo que es más importante, dado que se necesitan dos para bailar el tango, la concordancia de ID sólo puede funcionar si existe un doble consentimiento por parte del editor y del anunciante, lo que significa que las tasas de atribución IDFA son mucho más bajas.

La conclusión es que el IDFA sigue aquí, y aunque sólo está presente en una cohorte mucho más pequeña de usuarios, este grupo es muy valioso para la evaluación comparativa, la elaboración de modelos y las extrapolaciones en audiencias no consentidas.

Los mapeos de valores de conversión muestran las diferencias entre las apps de juego y las que no son de juego

El área principal con la que los marketers han estado luchando este año fue averiguar cómo trabajar con el mecanismo de valor de conversión SKAdNetwork de Apple.

Más concretamente, cómo aprovechar al máximo los datos limitados, ya que son los únicos datos posteriores a la instalación que pueden conectarse a sus campañas. A pesar de las limitaciones, es primordial hacerlo bien.

Lo que podemos aprender analizando los datos del Conversión Studio de AppsFlyer es que las aplicaciones de juegos se centran en los ingresos, y como tal, es un modelo que está involucrado en la mayoría de los esquemas de valor de conversión.

Su configuración más común es la de Eventos e Ingresos, con un 36%-48%, a excepción de las aplicaciones hipercasuales que prefieren las configuraciones de sólo eventos (38%). La configuración de solo ingresos también es muy popular entre las aplicaciones de juegos, con un 18%-35% que optan por este esquema.

Por lo que respecta a las opciones que no son de juego, la opción más configurada es la de eventos, mientras que la de compras alcanza el 40%, la de finanzas el 56%, la de salud y bienestar el 58% y la de entretenimiento el 57%.

Para saber más sobre cómo aprovechar al máximo los valores de conversión, incluyendo los benchmarks sobre el temporizador de la ventana de actividad, y el uso óptimo de la capacidad de 64 combinaciones, haz clic aquí.

Lo que nos espera en 2022

Las tasas de suscripción seguirán mejorando a medida que los usuarios se den cuenta de la mala experiencia de uso que obtienen de los anuncios no dirigidos, mientras que las marcas mejorarán en la optimización de sus avisos y ofrecerán un claro intercambio de valor.

¿Aún no estás convencido? Un nuevo reporte de Gartner predice que las tasas de opt-in aumentarán en más de un 150% para 2023.

En cuanto a los valores de conversión, con el tiempo, el conocimiento, las pruebas y la formación, los marketers afinarán su mapeo y sus esquemas para sacar el máximo partido a los datos de que disponen.

Recibe en tu bandeja de entrada las últimas noticias de marketing e insights de expertos

En resumen

Los cambios en 2021 en la privacidad han sido grandes para los usuarios finales y la importante causa de proteger sus datos, pero no tan grandes para los marketers.

Pero – las cosas están mejorando a medida que nos dirigimos a 2022 y más allá:

- El aprendizaje continuo de SKAdNetwork, las nuevas funciones de Apple, las soluciones de redes publicitarias y la innovación maximizarán el valor de SKAN

- La optimización de la tasa de inclusión ayuda a aprovechar los IDs de los dispositivos de los usuarios que han dado su consentimiento -cuando proceda- con fines de modelización y evaluación comparativa

- La innovación que preserva la privacidad mantendrá la mensurabilidad (por ejemplo, modelos de aprendizaje automático, incrementalidad, etc.)

- La colaboración de datos con preservación de la privacidad dentro del ecosistema basado en las tecnologías de Data Clean Room introducirá una nueva y mejorada forma de permitir las actividades de marketing que marcará todas las casillas:

- Información a nivel de usuario en formato agregado para la optimización

- Mejora de la experiencia del usuario

- Protección de la privacidad de los usuarios

BONUS: El crecimiento interanual por categoría y país muestra que las apps de finanzas están en expansión

Una comparación de categorías nos muestra otro ángulo de lo diferentes que son iOS y Android en 2021.

Los cambios en la demanda general de aplicaciones variaron significativamente entre las dos plataformas en casi todas las categorías, especialmente Citas, Noticias, Compras, Finanzas, Salud y Estado Físico y Juegos.

En términos de crecimiento puro, como hemos mostrado en nuestro reporte anual sobre el estado del marketing de las aplicaciones financieras, las finanzas están en un momento álgido con la tasa más alta en iOS y la segunda más alta en Android.

Las fintechs están por todas partes, ayudando a la gente a gestionar sus finanzas personales, a invertir en acciones, a gestionar carteras digitales, métodos de pago, criptomonedas, liderando una revolución global en la relación entre las personas y su dinero.

Las redes sociales y las compras también han mostrado un crecimiento impresionante, mientras que los juegos se han quedado atrás debido a las pérdidas en iOS (Lee más arriba).

Los mercados en desarrollo impulsan el crecimiento

Un análisis al mapa del mundo muestra muchos mercados de hipercrecimiento con una tasa de crecimiento del 30% o superior en el mundo en desarrollo a través de América Latina (Perú, México, Colombia, Brasil), Oriente Medio (Irak, Argelia, Egipto), África (Nigeria, Sudáfrica), el subcontinente indio (Bangladesh, Pakistán, Nepal) y el sudeste asiático (Filipinas, Indonesia).

Por otro lado, el crecimiento en EE.UU. quedó rezagado en comparación con otros mercados, pero aun así consiguió aumentar la demanda de aplicaciones (+10% interanual), mientras que las instalaciones en otro megamercado, la India, crecieron un 14%.