The pandemic-accelerated rise of mobile, coupled with more available options than ever before, demand from consumers with more mobile accessibility and expectations for top notch service on the go — have all driven financial brands to emphasize mobile finance and at user’s fingertips whenever the need arises.

This one-way digital trend did not skip the realm of Fiserv. Mobile finance, including a suite of activities like banking, investing, trading, transferring peer-to-peer — has become a lot more personal, and at user’s fingertips 24/7.

What are the main subcategories of finance apps now available?

Banking – One of the largest subcategories, banking apps are the efforts of traditional banking institutions to keep up with mobile demand.

They are distinguished from other finance apps given the stricter regulations under which they operate and their regular usage, with examples including US Bank, and JPMorgan Chase.

Wallet / peer-to-peer – This subcategory includes apps through which users can make and receive payments, allowing them to replace physical currency for digital.

The number of these apps is currently low, but they are being adopted at increasing speed, particularly in Asia Pacific, with examples including Paytm, and Square.

Money lending – These would be apps through which users are connected to investors, either peers or businesses — that offer a variety of loan options.

It’s one of the largest types of personal finance apps, especially because many loans distributed via this channel don’t require the same level of regulatory qualification as from more established institutions, which makes them relatively easier to obtain. Examples include Quicken Loans, and Borrowell.

Trading / brokering / investing – Apps through which users have access to an in-app trading or investment portfolio. A smaller but emerging subcategory, trading or investing apps make long-term investment accessible to users who may have fewer assets to contribute, or little knowledge about healthy market engagement. Examples include Stash, and Plus500.

Note that, for the purposes of this guide, any distinction between these subcategories will be made more generally between Banking and Personal Finance apps, which include the latter three.

As we can see, mobile finance is taking off. In fact:

Users worldwide tend to check their bank accounts around 7 times a week.

Finance apps spent $3 billion on user acquisition in 2020, and no less than $1.2 billion in Q1 of 2021 alone.

The general mobile finance sector is processing an impressive $1.3 billion daily.

Stemming from this growth, several key trends have emerged:

The banking of the unbanked, reaching a growing amount of one-fifth of the world’s population (largely in developed areas) that do not use financial services.

Increased replacement of traditional in-person services with mobile, especially in the US and among millenials. A recent Facebook report showed that 47% of current app users aged 18-34 in the US want the ability to conduct all retail banking actions digitally.

Significant mobile finance habit building as a result of app stickiness.

“Increasingly, we trust mobile apps with our most sensitive information and are engaging with retail banking brands more frequently than ever before across the board.”

While finance apps can play a key role in deepening brand loyalty, driving account registrations, and improving product sales, there are also multiple challenges to overcome:

1 – Privacy and security around 3rd party data sharing

In general, the data collected and maintained by finance apps is largely more sensitive than for other verticals.

That being said, the biggest security regulations are faced by banking institutions, who are governed by the strictest regulatory bodies and must naturally hold on to user data for longer periods of time.

Over the past few years, privacy has taken center stage in mobile app marketing, and particularly for iOS (Android’s changes are at least two years away).

Apple’s introduction of the ATT prompt, which severely limited the availability of its unique identifier, the IDFA. As a result, user-level data has become much less readily available.

These privacy-centered changes have a direct effect on marketers’ ability to measure LTV, remarketing campaigns, and segment audiences. Luckily — innovation is continuing to lead the measurement front with confidence, as data shows it has been largely restored to pre-ATT levels.

2 – Securing conversions for sensitive functionality

While the emergence of finance apps has completely transformed the way many consumers handle their finances, the stakes are still higher for marketers to get users to convert due to the sensitive nature of such functionalities.

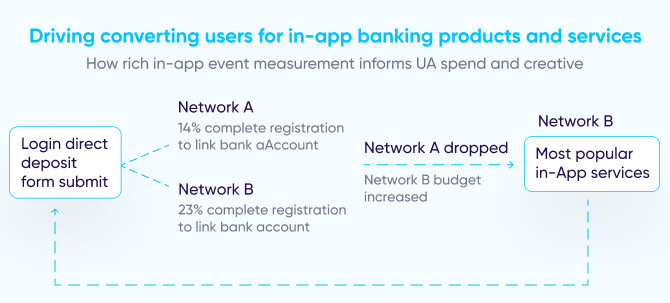

Although marketers may often have CPA models calculated on such actions as linking a bank account (for Fintech apps), completing in-app account registration, or a web-to-app transition (for traditional banks), it’s simply difficult to secure user conversions.

Reasons vary from the “non-traditional” app environment for certain functionalities, to security concerns.

3 – Optimizing the conversion flow and unifying the customer experience

As the number of touchpoints in a user journey increases, so does the possibility of friction or drop-off between them.

Instead of adding more, it’s more important for marketers to not simply connect the dots, but to optimize existing ones with data. Many Finance apps have dedicated teams for such optimization, and drive these efforts with strong hypotheses.

4 – Fraud

Among all verticals, finance was the 2nd hardest hit category in 2021 in terms of fraud (38% app install fraud rate) due to its massive scale (3rd largest category) and higher than average payouts ($3-4 CPIs).

Note that fraud in finance apps is more centered around registrations than installs, since installs are not usually the primary value conversion for most marketers.

5 – Connecting the dots

As mentioned above, the journey of a mobile finance consumer often spans across multiple devices, platforms, and channels. This is because of online and offline ad exposure and the availability of multiple touchpoints.

For more traditional financial firms, such as banks, the main challenge comes from bringing an extensive existing user base from web to app.

For emerging mobile-first companies, however, like digital investment tools or wallets, the main cross-device focus is on strengthening their web presence in order to drive mobile engagement via web ads.

Therefore, the diversity of paths in the vertical dictates that connecting the dots between these different touchpoints, and making sure you’ve linked the right data to your app — can be a real challenge.

Working with an effective measurement and attribution provider can help bridge the gap and give you your true user LTV.

6 – Engagement of existing users

Especially true of banking institutions, apps are not primarily used as a destination for user acquisition.

Instead, they’re used to convert existing web or offline users to mobile users, improve the user experience, and diversify user touchpoints available via funnel-based audience segmentation and deep linking.

For companies predominantly working with other, more traditional channels, this shift may prove challenging.

7 – Personalization

Delivering a personalized user experience is key for driving users to engage with specific functions within an app, primarily when a company has more than one focus (i.e. banking, investment, and retirement offerings).

This can be done through deep linking, push notifications, and targeted advertising.

However, personalization is not as important for many finance apps, since there is often only a single functionality within them to which users may be directed.

Additionally, while the reward of converting mobile finance users is high, marketers must balance between respecting user privacy in the era of GDPR and ATT, increased regulatory scrutiny due to the sensitivity of the data, and meeting user expectations of a personalized app experience.

The solution: Granular measurement as the foundation for… everything

One golden truth of app marketing is that there are no strategies and processes without measurement and optimization. Not only of basic KPIs, but also granular metrics that map every stage of the conversion funnel to inform both user acquisition and re-engagement.

In turn, marketers are able to hone in on the users they’re looking for and uplift their overall marketing performance.

Before you even get started in setting up your UA campaigns, you must first have a few capabilities in place to guide your setup in the right direction. Let’s take a look at the essentials:

#1 – Event Mapping

To begin discussing the importance of granular measurement for successful UA, let’s take a deeper look at what that actually means in practice.

The chart below explores some of the main metrics savvy finance app marketers measure to optimize their efforts and deliver the highest-value users to their apps. The left column contains vertical-specific goals, while the right column contains the metrics through which these goals can be met.

Goal

KPI

Installs related • Acquisition • Cost

• Organic / Non-organic split • Month over Month growth (non-organic) • CPI / CPA • ROI

Conversion related • Registering users • Reduce friction in registration flow • Loan application

• % Click to install rate • % Install to Complete Registration rate • % Complete Registration to Link Bank Account rate • First loan

Engagement related • Stickiness • Short term loyalty (less important than long term) • Long term loyalty • Mobile-only feature offerings

DAU / MAU • Retention D1, D7, D30 • Week 8, week 12 retention rate • Uninstall rate day 7, day 30, day 60

Connecting the dots • Web to app user conversion

• Unique new users (app brought in, did not interact with other touchpoints)

Note that, although all metrics above are important for improving the profitability of your app, engagement metrics in particular are not as important to marketers, since average and “healthy” usage of finance apps is likely to be lower than in other verticals.

For example, a mobile banking user might only login to check their account once a week or month, versus a gaming app user who plays on a daily basis.

What to measure – SKAdNetwork

One of the most complicated aspects in Apple’s iOS 14+ measures to safeguard user privacy — is SKAdNetwork’s conversion value and timer extension mechanisms. Since post-install data is what matters most in the freemium-driven app ecosystem — this poses somewhat of a problem.

Before iOS 14, marketers could measure in-depth and at length to determine user or campaign value. But in Apple’s SKAdNetwork, data is far less in-depth. You get 64 combinations from 6 bits to map post-install activity and a few days at best of activity data. In other words, conversion values are SKAN’s alternative to [limited] LTV.

With limited options, it’s imperative that advertisers make the most of what is possible. To be clear, what is possible can be plenty — if done right. But what does ‘right’ look like? How should marketers map their conversion value schemes?

To answer this question, we looked at data from our recently released Conversion Studio and analyzed the configurations of 600+ apps to help advertisers learn the bits and bytes — about the bits and bytes.

The data shows that for many marketers, conversion values are tough to master. While some have learned to squeeze the data lemon (unsurprisingly, mainly from the gaming crowd), others are not even close to utilizing the full potential of this new mechanism.

For more SKAN Insights, visit the Inside SKAN series. And for a recap of what conversion values are all about — here’s a quick video.

The why and how of rich in-app events

The depth to which we can gather the right data in order to optimize campaigns towards high quality users, and boost engagement and revenue along the way, is significant.

That also means the amount of data we need to handle and analyze is massive, though with the right tech stack, setup, and attribution platform, marketing analytics can be made much easier.

But still… Why do I need to measure rich in-app events and other granular data?

Highly effective UA, engagement, remarketing — are all driven by building audiences and optimizing media sources, channels, campaigns, and creatives based on rich in-app events.

These events add layers of both available and measured parameters that map out ideal user behavior.

With the raw data you receive from a measurement and attribution provider, you’ll be able to actually see user trends and patterns you might otherwise miss. It will help you to get a complete picture of user activity and behavior, no matter the platform, channel, device, and the time at which they perform actions.

For example, many traditional banks are most concerned with providing value and service recommendations to existing clients, so optimization will focus on driving users to more of those assets, customized based on individual need and engagement history.

For personal finance apps (e.g. investment, payment, and financial management), monetization happens from in-app actions and payments, as well as from affiliate revenue, where apps successfully recommend users to related products and services from other brands.

Let’s look at the top events banking and personal finance marketers typically measure:

Banking:

Login

Direct deposit / Transfer

Page view

Application / Form submit and completion

Personal finance:

Registration

Linking (bank account, credit card)

Deposit

Application / Form submit and completion

Note: In general, finance apps aren’t as concerned with granularity and the qualitative information of events as much as with the quantity of users within each event.

This is primarily due to the strict regulatory bodies and requirements under which they operate. As for any app, granular placeholders are available within an attribution platform to those who need it, but in general, they are not as widely used in this vertical.

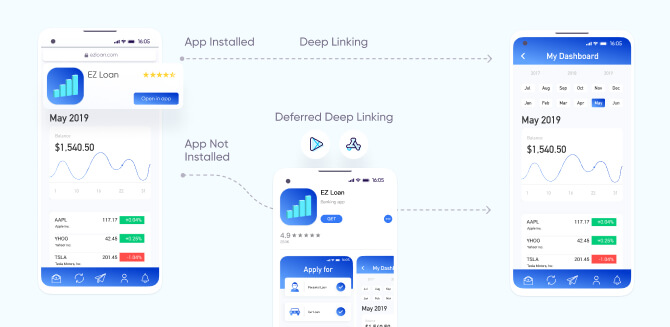

#2 – Deep linking

One of the most powerful tools in the app marketing tech stack is deep linking, creating a contextually-relevant user experience across channels, platforms, and devices. How is this done?

Using the information contained in the deep link, users are brought directly to a specific product or campaign landing page within an app, seamlessly moving from promotion to the app landing page with greater likelihood for conversion.

In the financial services vertical, deep links are most often used to drive customers to pages to check on their balance, investment performance, or product and services pages — based on previous viewing behavior.

To get started, you must first configure deep linking. Luckily, this can be done easily by implementing code in your app, or through enabling associated domains, depending on the method used.

Also pay attention to the fact that deep linking is needed for both specific product, service, application, registration, or other account pages.

The destination to which a user is brought is primarily dependent on:

The deep linking campaign goals

The consenting user information previously gathered (i.e. content viewed, account history, location, etc.), which must be decided and understood ahead of time.

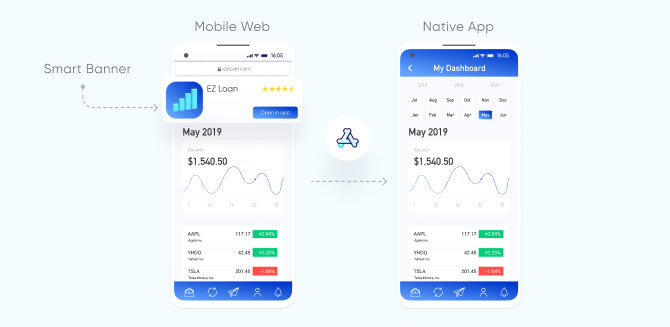

Well-rounded finance app marketers use deep links to bring existing and converting users specifically from mobile web to their apps — via an ‘Open in App’ call-to-action smart banner.

These call-to-actions often go hand-in-hand with campaigns offering special offers or benefits for in-app users, or service suggestions based on previous web engagement history.

Through the deep links placed in these banners, marketers can bring new users to install their app, get smoothly routed to the same product or service page previously viewed, and later to a form page for signup.

But why would marketers want to reroute users to their app from mobile web in the first place? Simply put, the app is the ultimate destination because of its unmatched native user experience, data insights, and massive brand impact it can provide by placing a logo on prime real estate — a user’s mobile home screen.

When a user clicks on a smart banner popup and follows it to a page in the app, you can receive data on the user’s subsequent in-app activities, the IDs of product and category pages visited, and even, retroactively, the attribution data from the user’s journey to your mobile website.

Beyond the valuable data gathered, however, smart banners also contribute to an improved user experience, increasing the potential of greater brand loyalty and engagement overall.

When choosing a deep linking solution, make sure that it not only supports your growth needs, but is also in sync with the latest privacy and security guidelines, and your campaigns comply with the most up-to-date user privacy and security regulations.

#3 – Uninstall measurement

It’s not enough to bring users smoothly to your app, and personalize their experience within it to optimize conversion rates and reduce churn.

Marketers must also address the inevitable segment of users who will uninstall their app completely, and either build a strategy to bring those users back to active engagement, or exclude these users from future campaigns — if they believe a re-install is unlikely to occur.

To do so first requires understanding why, when, and which users uninstall, especially given the rising scale of competition and higher user expectations.

So what are some of the things that can make users uninstall your finance app?

Poor in-app functionality and experience. Optimize your UA campaigns all you want, but it’s nothing short of critical to ensure you have a great infrastructure to support your app’s functionality, and ensure a flawless path to conversion.

Excessive and/or impersonal onboarding process. Ensuring that your users move as quickly and smoothly to active engagement as possible means building an onboarding process that is short, simple, and intuitive. |

It should cover app basics and potentially even offer incentives. One option is to conduct registration or sign-in via a Facebook or Google account.

Irrelevant or overwhelming notifications. While finance apps can use push notifications to update users on account changes or activity, offer incentives, share general news, or simply bring inactive ones back to a potential conversion — it’s also possible to overdo it.

Be intentional about sending only key notifications, at appropriate times, to users who display strong intent and relevant characteristics for each message.

It’s also important to note that, while churning users do pose a challenge to finance apps, it’s not as mission-critical to reduce as in other verticals. Many of the core functions within the app, such as applying for and receiving a loan, can be completed as one-off activities.

Given that users can uninstall your app for a combination of many reasons, understanding your app’s uninstall rate is extremely important. But what exactly are the main benefits of uninstall measurement for marketers? There are a couple:

Compare the overall quality of your media sources by exploring the performance and retention of users from different media sources, campaigns, single ads, countries, etc.

Protect user privacy by removing uninstalled users from retargeting segments and discontinuing re-engagement messaging.

#4 – Fraud protection

As mentioned in the introduction, fraud is a massive problem, particularly for finance apps because of their scale and high payout.

Despite significant improvements in anti-fraud solutions and growing awareness of the dangers of app install fraud, finance apps are still a hard hit vertical.

Unlike other verticals, however, fraud in finance apps is most often focused on registrations or other down-funnel conversions, rather than installs. That’s because marketers are looking for active users that are regularly managing their personal finances or making investments in-app, rather than simply a high scale of installs.

Increased fraud has led to much stronger protection, which in turn led fraudsters to up their game with increasingly more sophisticated fraud tactics.

This is especially evident in the use of bots that mimic in-app user behavior in an attempt to bypass protection, or from device farms — that include either thousands of actual devices on racks or virtual, emulated devices.

A good anti-fraud solution uses a blend of supervised and unsupervised machine learning driven by a large scale of data.

For more information about how AppsFlyer uses both machine learning and big data to combat fraud — read here.

Advanced protection

One challenge facing effective app install fraud prevention in the finance vertical is awareness of the issue and a more sophisticated understanding of the threat it poses.

Given the nature of data in this vertical, “fraud” is more often associated with functionality and content-related deception. That is, companies and users alike might think about facing money-related loss from accounts and other theft, rather than also consider the inevitable risk and financial exposure of their app and devices.

Another common myth is that CPA-modeled finance app campaigns experience little to no fraud — due to the lack of install-focused incentive or the difficulty of generating an in-app event (i.e. credit card verification, linking bank account, adding a valid address, etc.) for fraudsters.

That simply is not true. For this reason, the following factors contribute to detecting and preventing fraud:

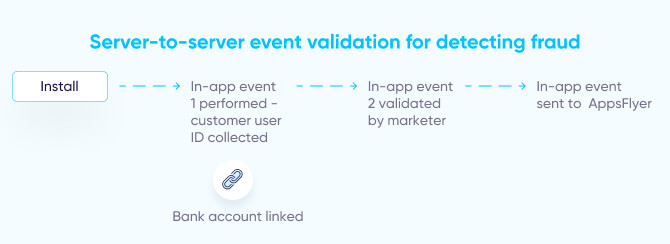

Server-to-server in-app event validation

For many finance apps, when an in-app event is recorded, only the fact that it happened (the counter) is sent to an MMP — without including any further details about the event (the values).

Savvy finance app marketers, however, will often send any event that is recorded to their own server to verify that it actually happened, or to collect more specific information about a user before sending the MMP that event.

For example, if a bank account link is recorded, checking this event server-side can tell the marketer which bank the user linked to or whether the link was successful, instead of simply relying on the record of the event and leaving a greater possibility for fraud.

Personally Identifiable Information (PII)

As mentioned above, the level of data sensitivity for finance apps is higher than in other verticals. While PII is not shared outside of the company’s own servers, it does play an important role in fraud detection and prevention, since account activity is always validated by name, address, social security number, etc.

Incremental lift

The measurement for any conversion consists of an organic and non-organic baseline, which is important to include in regular analyses — not only for determining media source performance, but also for preventative fraud detection. If the non-organic total is “increasing” at the expense of organic without raising the budget, it’s possible that the network isn’t adding actual value, and instead is using one or more methods of attribution fraud (i.e. click flooding and install hijacking).

#5 – Mapping a holistic customer journey

The reality is that a significant divide between user behavior and marketing measurement still exists in our day and age.

On one hand, finance end users have increasingly more complex conversion journeys involving multiple devices and touchpoints — desktop web, mobile web, apps, and offline, traditional banking.

On the other hand, marketers are measuring user actions across different channels and devices, but primarily doing so in silo from one another. Their data remains disparate and is analyzed by different teams. Their goals, strategy, and subsequent action are formulated and executed in parallel lines that rarely meet.

However, the good news is that customers are increasingly turning to mobile as the data-driven heart of the personalized digital finance experience, and more often staying exclusively there once adopted.

Still, marketing efforts and measurement technology can and should be built around the needs of omni-channel customers. The data capabilities of mobile, which has become the most easily measured ecosystem, allow marketers to bridge the gap between on and offline touchpoints, and unite each user across platforms with a single customer ID as part of the overall brand.

One growing trend for finance app marketing is the use of user referrals to connect the dots between different apps from a single brand.

For example, if a company has separate investing, retirement, and banking app products, they might create a measurable, incentivized referral program that allows existing users to share both that app and the related products with peers — for increased traffic and engagement.

Personalization of your user’s experience, when possible under privacy regulations, should be a priority, both in and out of your app. Emphasize a contextually relevant onboarding process that encourages users to register for an account and set their own preferences.

You can also use granular in-app event data to guide users to specific functions within the app, or suggest related products or services for greater upsell and affiliate revenue opportunities.

2 – Keep messaging simple

While personalization keeps ongoing mobile financial management relevant, it’s also important not to overcomplicate the messaging.

Given the diverse range of functions available within a single finance app, or across a related family of apps, be intentional about using targeted and engaging messages for maximum effect.

3 – The web-mobile combination

Despite the continued growth of mobile finance, some users still rely on desktop websites for their digital finance needs.

Particularly for mobile-first companies, it’s important to create a sustainable web presence to use as a strategic touchpoint, driving users down your funnel to relevant, specific functionality in which they’re most likely to convert.

4 – Segmentation sweet spots: Scale vs specific

Keep audiences broad enough to have sufficient scale for machine learning, but specific enough to find the unique users you’re looking for. Bear in mind that this cap will change per platform (Facebook, Google, etc.) and can also change over time.

5 – Follow the funnel

As a general rule, almost all marketing efforts, especially audience segmentation, follow the specific conversion funnel of the app, or suite of apps, given the diverse functionality offerings of mobile finance.

However, beyond keeping the app experience relevant for existing web or offline users, following your funnel also improves the collaboration and communication across departments, leaving less room for confusion and duplication.

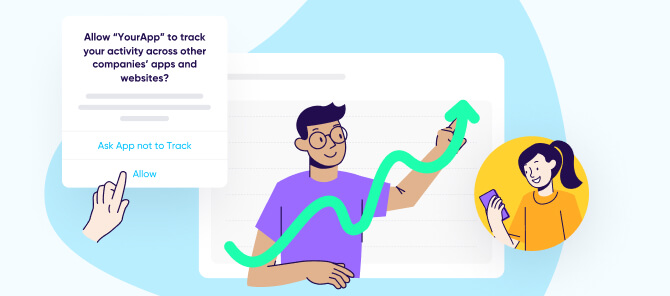

6 – Increase ATT opt-in rates

So far, ATT opt-in rates have been higher than many initially thought prior to the iOS 14.5 rollout, and currently range at around 47% on a global scale among users who saw the prompt (see interactive dashboard for more).

Based on our most recent data, here are 2 ways to increase your ATT opt-in rates, and reap the rewards of greater quantities of user level data and attribution:

Timing is everything – Show the prompt to installers on 1st launch

You have control over when to show the ATT prompt (or if to show it at all) — and your decision can have a significant impact on opt-in rates.

According to our data, opt-in rates are at their highest when users launch your app for the 1st time — likely among other in-app notifications. And the sooner the better:

As you can see in the Days tab, the share of IDFA rates in Finance apps drops from an average of 47% upon launch to 41% from day 1 onward. Not a huge gap, but enough to make a difference.

As for the Minutes tab, the reason behind the dramatic spike stems from the fact that the attribution SDK is triggered before the prompt is served, which could be a matter of mere seconds. To avoid this, it’s recommended to synchronize your prompt with your attribution’s SDK trigger, and ensure that it’s triggered shortly after the prompt is shown.

When attribution occurs using IDFA, it’s important to send it during the 1st launch. The MMP’s SDK can “wait”, which allows marketers to configure how long the SDK should defer for the ATT status, before the data is sent to the MMP’s servers.

Offer a post-ATT in-app notification to your engaged, non-consenting users

For users who decline to give permission when shown the ATT prompt, it doesn’t need to be the end of the road. They can still enable permission tracking at any time (and disable it again, if they wish) in their device’s Settings.

That said, your users might not know this, so — this is your chance to give them a reminder. As with the pre-ATT prompt, show engaged users a post-ATT notification that includes the user benefits of opting in, which will take them directly to their Settings for app opt-in.

About 30% of Finance apps show at least 10% higher IDFA rates on day 2 compared to day 1. This could be either because these apps served their prompt to some engaged users on day 2, or because they served it during the 1st launch and then showed a post-ATT in-app notification to their engaged users on day 2.

7 – Make the most of your SKAdNetwork Conversion Values

Having 64 options in your SKAN campaigns might sound limiting, but it still offers plenty of value if the bits are properly allocated and utilized.

Make the most of ranges and combinations and focus on the post-install actions that matter most. Test, test, and test again until you find the right mapping (having a UI certainly makes it easier).

Also, take advantage of Funnel measurement, which can be a more efficient way to allocate your bits. Instead of dedicating 3 bits to measure 3 separate events, a funnel configuration can measure sequential behavior using only 1 bit.

Mobile measurement solutions in the era of user privacy

Finance app owners can now turn to a host of new and not so new solutions to be able to regain granular, actionable insights. These include:

SKAdNetwork – Apple’s deterministic aggregated attribution solution. Within this framework, SKAN conversion values allow marketers to grade user value after the install.

User-level deterministic attribution – ATT opt-in rates surpass 50% for many finance apps (among users who saw the prompt). Not only isfull data granularity enabled for these users, but also the ability to segment towards non-consenting audiences.

Aggregated probabilistic modeling – a statistical technique that leverages machine learning to estimate campaign performance with a high level of accuracy.

Predictive analytics– allows marketers to make data driven decisions about users’ future value with a high level of confidence, while relying on very limited data points early in the funnel.

Top-down measurement – holistic methodologies such as Incrementality (identifying incremental revenue drivers in order to optimize budget allocation), and media mix modeling or MMM (measuring the impact of campaigns to help determine how various elements contribute to the bottom line).

Data Clean Rooms – enabling privacy-compliant measurement and optimization in a highly secure, permission-only environment where advertisers can leverage user level data insights without access to user level data.

Chapter 3

Re-engagement – What to measure and set up

Having a successful finance app is not just about acquiring new users and driving them to conversion. It’s also about making sure those who arrive remain engaged over time, ultimately driving revenue and lifetime value.

This is certainly true for finance apps, who enjoy higher average retention rates than other verticals — despite a 18.4% drop on day 30 compared to the previous year.

At the same time, they also face particular difficulty driving sustained and frequent engagement.

Many users download banking apps but don’t regularly engage with or understand their full capabilities. Because of that, re-engaging this vertical is largely about bringing lapsed users back to the app to drive account activity and long-term engagement.

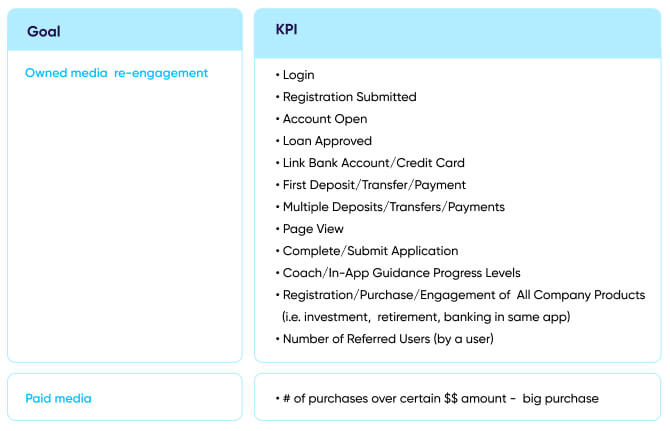

1 – What to measure

Below are the main metrics top finance apps include in effective re-engagement, with the left column containing vertical-specific goals, and the right column containing the metrics that indicate and drive these goals:

2 – ROX, deep linking, and great CX

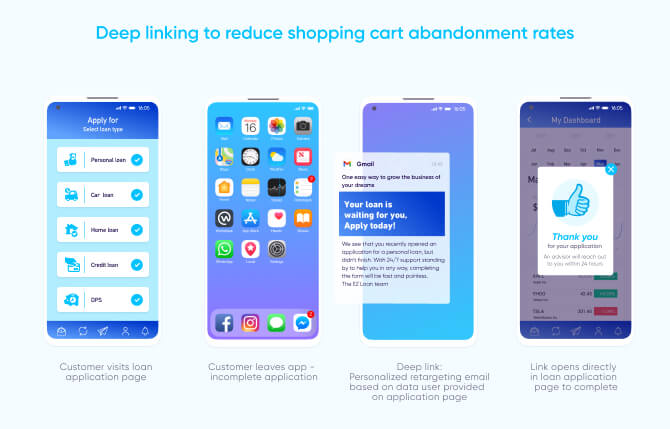

We addressed earlier the why and how of deep linking in acquisition, but in the finance vertical, deep linking is just as vital for re-engagement and remarketing.

For finance apps that tend to have longer and higher-value conversion cycles, it’s easy for users to become inactive or even uninstall before and sometimes after registration, application, or conversion.

Marketers must be especially proactive and keep users steadily engaged after install, rather than face the more difficult task of bringing them back after they’ve already jumped ship.

Deep linking is often used in conjunction with email and push notifications, given the critical level of personalization this messaging requires. That said, deep linking also enables paid campaigns personalization, which is how you’re served an ad with the pair of shoes you looked at instead of some general creatives.

For example, emails with deep links embedded in CTAs leading to product X’s registration or application page might be sent to users who visited product X information page in the app, but didn’t register.

Likewise, for users who did register for product X, an email containing deep links might bring this segment to related product or service pages that pair well with product X.

For finance apps in particular, deep links can also be used to set up a user referral program, which can be used to drive users to specific functionality within a single app, or to different products within a family of related apps.

The analytics from these links allow marketers to measure both the number of users referred as a result of a single link, and the number of new users a given customer was able to successfully bring to the app. These metrics are then applied to further remarketing campaigns that employ incentives for richer engagement.

So, by offering great CX, marketers are able to take more users to their desired destination and widen the bottom of their funnel. Product managers, on the other hand, can leverage deep linking to better engage and retain their users.

Great CX leads to business results, and the business impact resulting from investment in customer experience is known as return on experience (ROX).

To learn more about ROX and how it can propel your app engagement forward, have a look at our ROX guide.

3 – Owned Media

Owned media is any marketing asset directly controlled by a company and which requires little to no additional cost to access and use. Most relevant to mobile re-engagement are push notifications, emails, and SMS messages, but also webinars and tweets.

Owned media is your way of creating free, contextual content designed to increase engagement on your active, idle or lapsed users’ side — and create a more personal, long-lasting connection. In the age of user privacy, where user-level data is harder to come by, this connection is nothing short of critical.

Let’s explore this process. Usually, marketers have a CRM which enables the use of such campaigns. These CRMs receive data in two ways: either through their own SDK, or through an attribution and measurement provider.

The latter typically has pre-built integrations with the most popular tools worldwide, allowing marketers to export their data directly.

Imagine that a user began the onboarding process of creating an investment portfolio, but didn’t link a bank account or select their investment preferences. Based on these in-app events (which the CRM receives), the marketer first runs a push and then an email campaign, but the user still doesn’t finish building their portfolio.

At this point, the marketer might either start remarketing via paid sources to drive conversion, or add this user to an audience segment for future remarketing exclusion.

If the marketer is savvy, they will use different parameters to run diverse campaigns by mobile finance product, on push, email, and paid channels. For lower value products, leveraging owned media makes complete sense because it’s practically free.

For high value products, however, marketers can also re-engage using paid media. Interestingly, despite their widespread use, many marketers are still not fully aware of the long term value these channels inevitably provide.

Why leverage owned media?

Utilize the marketing “hierarchy.” Given the little to no cost of owned media channels, especially compared to paid campaigns, re-engaging users via these channels should be the focus and priority as much as is possible and appropriate.

Performance anomalies. In the event of sudden growth in the number of purchases or other metrics, you might not always understand why. Measuring your owned media alongside paid allows you to pinpoint if a particular growth anomaly came from a specific channel or partner, and subsequently decide where to further allocate budget.

Creative optimization. Particularly relevant for campaign managers, if a creative or ad is connected via deep link to an email or push notification, measuring these campaigns will specifically identify which creatives are delivering the best results.

4 – Remarketing via paid media

Because finance apps face longer and higher value conversion cycles, re-engaging lapsed or uninstalled users (or alternatively excluding uninstallers from your campaigns) is necessary for ensuring long-term retention and lifetime value.

Additionally, given the challenge of increasing UA costs, it’s cheaper to proactively re-engage your existing users, driving them from desktop and mobile web to app, rather than acquire new or lapsed ones.

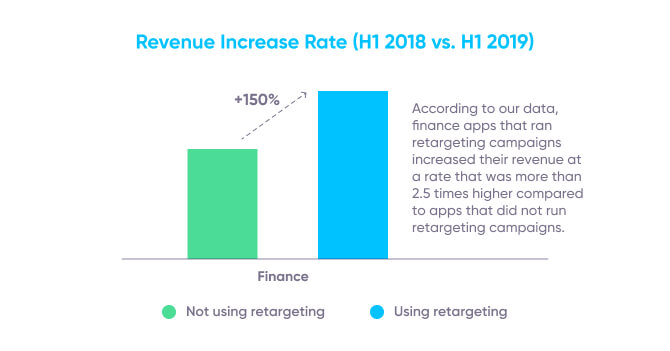

In fact, according to our recent re-engagement guide, there’s a 2.5x increase in the number of remarketing conversions among worldwide apps running global campaigns.

One of the most common remarketing segments, and often the start of full funnel remarketing campaigns, is the group of users who install but don’t proceed to link their bank account or complete account registration.

As the base for most of the subsequent activities users can complete in-app, it’s especially important that they complete this action before further engagement.

Given the amount of information companies can receive from the user onboarding process, these campaigns can start with owned media campaigns, primarily email and push, in order to maximize conversions while minimizing spend.

Timing remarketing campaigns

Deciding when to start running remarketing campaigns depends on multiple factors, such as the type of audience segment, your budget, level of engagement, and whether you’re seeking to recover users or simply re-engage.

Remarketing campaigns may be launched as early as immediately or 24 hours after install, within the first week, or later. There’s no one-size-fits-all formula.

Stopping your campaign also depends on several factors, not the least of which are your expected marketing goals and the limits of your campaign budget.

In the finance vertical, marketing experts tend to end campaigns after 7, 14, or 30 days, though one perspective says that the remarketing window is best determined by the length of the desired conversion cycle for the majority of your organic users.

Because of that, it’s important to ensure that however long you run your campaigns for, be sure to stop them within a reasonable amount of time to avoid putting your budget to waste.

Chapter 4

Best practices for effective remarketing

1 – Re-engagement audience segmentation

As in acquisition, your granular in-app event user data can be directly applied to create audience segmentations for re-engaging users. Push notifications, emails, and other owned media are most often used first in re-engagement campaigns given their low costs and ability to reach users more easily than paid methods.

Below are some examples of audience segments for re-engagement:

Retarget and re-engage. Improve your re-engagement by targeting high-value users who made multiple purchases or conversions last month, but were inactive this month.

Recover or deprioritize uninstalled users. Target users who completed a certain number of lower funnel actions but who recently uninstalled your app with custom creative to drive re-installs. Conversely, you might choose to lower the priority of retargeting campaigns focused on these users and invest in audiences who are more likely to guarantee a higher value.

Cross-sell and upsell. Encourage users with high purchase intent to complete the original transaction with the addition of related products or services from that brand or others.

Remarketing exclusion. An audience who has engaged with a specific owned media source (push, email, SMS, other), or has met some other exclusion requirement (i.e. rejected for a loan more than twice), is excluded from paid retargeting.

Funnel completion. As users move through the conversion funnel, it is inevitable that they will drop off at various stages along this journey. Create segments for each of the actions users should complete in order to find those that aren’t progressing and drive them along your funnel to conversion.

Another important use of audience segmentation is the creation of split audiences for determining the incremental performance and growth of each media source, as well as performing A/B testing and pushing product features.

For the purposes of incremental and A/B testing, these split audiences can be based on the following factors, among others:

Action – Users who installed the app but didn’t convert yet

Exposure – Users who clicked an ad but didn’t install

Geographical distribution – Users located in a specific country

With incrementality and A/B testing, you can create two groups of users (test and control) across different networks and see which network, campaign, ad, or creative results in a more positive business impact.

Likewise, incrementality testing informs whether or not adding a new network to your existing portfolio has a true incremental impact:

1 – Product-specific assets

These should be created for each action for which you’re re-engaging users. Be sure to design a separate landing page with action-specific creatives and messaging that will serve as the homepage for each campaign.

For example, the messaging for a segment driving users to link their bank account or credit card, should be different than that of a regular homepage.

You should also always A/B test your creatives to understand their true impact. For high language affinity segments, be sure to use communication in the relevant local languages.

3 – Simultaneous creative testing

When it comes to optimizing ad and creative performance, testing 3-5 different creative sets simultaneously will provide the most profound performance analysis within a reasonable and efficient time period.

However, as a general rule, it’s better to test several different creatives more frequently than to perform tests on large amounts of creative sets at the same time.

4 – Personalization – not just for UA

With the sophistication of marketing tech and the number of available apps increasing, app users, especially in mobile finance, expect customized experiences from start to finish.

Use purchase or view histories to cross-sell and re-engage lapsed users. Pair deep links with other in-app event data to reduce incomplete purchase, registration, or conversion rates. Choose ad partners that offer behavior or intent personalization and make this process part of your marketing routine.

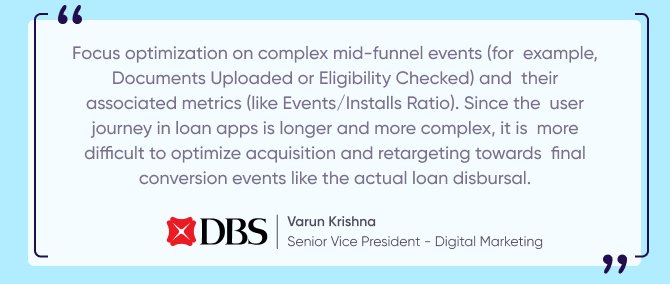

5 – Early funnel optimization

Focus optimization on complex early funnel events (for example, Documents Uploaded or Eligibility Checked) and their associated metrics (like Events / Installs Ratio).

Since the user journey in loan apps is longer and more complex, it’s more difficult to optimize towards final conversion events like the actual loan disbursal.

Final thoughts

Final Thoughts

In this stage of overall digital finance growth, mobile finance companies have more factors on their side to reach their business goals.

A pandemic-accelerated mobile explosion and a growing demand from consumers to save both time and money — has driven a rise in technologies which have greatly enhanced the mobile finance experience across platforms, without compromising users’ privacy.

It’s now easier than ever to make purchases, complete applications or registrations via mobile devices and, combined with promises of increasingly faster connectivity, mobile finance marketers are well-positioned to advance.

Facing this growth, the bottom line takeaway is the importance of granular measurement to carry marketers forward. Follow the suggestions and metrics as detailed above, and you will build the foundation for future profitability, performance, and success.